The U.S. Economy will grow 1.4% in 2023, after registering a 2% increase in 2022, the International Monetary Fund (IMF) projected.

After that, in 2024, U.S. GDP would grow 1%, according to IMF forecasts.

With a pickup in growth in the second half of 2024, growth in 2024 will be faster than in 2023 on a quarter-over-quarter basis, as in most advanced economies.

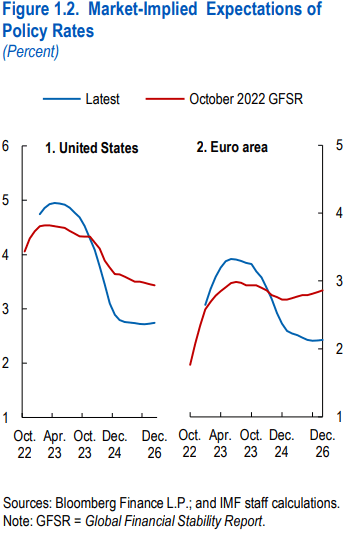

There is a 0.4 percentage point upward revision to annual growth in 2023, reflecting the carryover effects of domestic demand resilience in 2022, but a 0.2 percentage point downward revision to growth in 2024 due to the Federal Reserve‘s steeper path of rate hikes, to a peak of about 5.1% in 2023.

U.S. economy

From the IMF’s perspective, monetary policy is starting to make a dent. There are signs that monetary policy tightening is starting to cool demand and inflation, but the full impact is unlikely to occur before 2024.

Headline inflation appears to have peaked in the third quarter of 2022.

Fuel and commodity prices have come down, reducing headline inflation, especially in the United States, the euro area and Latin America.

But underlying (core) inflation has yet to peak in most economies and remains well above pre-pandemic levels.

It has persisted amid the side effects of previous cost shocks and tight labor markets with solid wage growth, as consumer demand has remained resilient.

Inflation

Overall, medium-term inflation expectations remain anchored, but some indicators are on the rise.

These developments have led central banks to raise rates faster than expected, especially in the United States and the eurozone, and to signal that rates will remain high for longer.

Core inflation is declining in some economies that have completed their tightening cycle, such as Brazil.

Meanwhile, financial markets are showing great sensitivity to inflation news, with equity markets rallying following the recent release of lower inflation data in anticipation of interest rate cuts, even though central banks have signaled their determination to tighten policy further.

With the spike in US headline inflation and the acceleration of rate hikes by several non-US central banks, the dollar has weakened since September, but remains significantly stronger than a year ago.