The Organization for Economic Co-operation and Development (OECD) expects Mexico’s budget deficit to increase to 3.1% of GDP in 2022, from 2.9% in 2021.

The OECD also projects that this deficit will then decrease to 2.8% of GDP in 2023.

It considers that the official measure of public debt will stabilize at around 50% of GDP.

From this Organization’s perspective, the ongoing recovery and medium-term growth prospects could be strengthened by increasing public investment, based on a cost-benefit analysis, and targeted spending on social programs.

The commitment to debt sustainability could be maintained by gradually broadening tax bases, phasing out inefficient and regressive exemptions, and strengthening the property tax.

To respond to rising inflationary pressures, the central bank has raised interest rates at its last nine board meetings, leaving the rate at 7.75 percent

With widespread price pressures expected to persist, further interest rate hikes are warranted.

The Mexican government has taken steps to mitigate commodity price pressures, including eliminating tariffs on commodities, cooperating with the private sector to freeze prices on 24 key products (mainly food) for six months, measures to increase production of basic grains, and reducing customs duties on commodities.

OECD

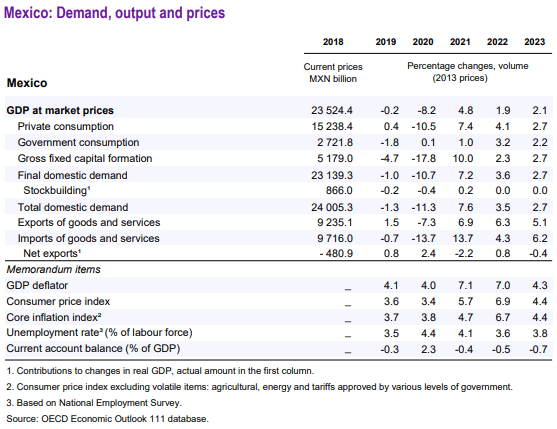

After weak performance in the second half of 2021, real GDP grew 1% (in seasonally adjusted quarterly rates) in Q1 2022.

While auto production remains constrained by supply chain issues, non-durable goods consumption is well above pre-pandemic levels, while services consumption and private investment lag.

Although unemployment and underemployment have declined, they remain above pre-pandemic levels.

Global inflation, supply chain disruptions and domestic factors continue to exert significant pressure on both headline and core inflation.

Consumer prices rose 7.7 percent year-over-year in April 2022, and core inflation reached 7.2 percent.

Twelve-month inflation expectations have continued to rise, but longer-term inflation expectations remain stable.

Boosting public investment and social spending further would deepen the recovery. Measures to respond to

increases in energy prices should be temporary and targeted at the most affected households and SMEs.

![]()