The Semiconductor Industry Association (SIA) highlighted five key facts about the U.S. semiconductor industry.

These facts were presented as part of a letter the SIA sent to the U.S. Trade Representative (USTR). Additionally, they were part of the ongoing Section 301 investigation.

The inquiries relate to actions, policies, and practices of certain economies concerning structural overcapacity and production in the manufacturing sectors.

U.S. Semiconductor Industry

According to the SIA, the Trump Administration’s agenda on market opening, trade, and investment plays a critical role in supporting continued U.S. leadership in semiconductors. This is achieved in part by creating new demand and facilitating sales of all types of U.S. chips in foreign markets.

U.S. semiconductor companies rely on access to foreign markets to sell their products.

In the course of this and other relevant Section 301 investigations, the SIA asked the USTR and other relevant agencies to consider the following points:

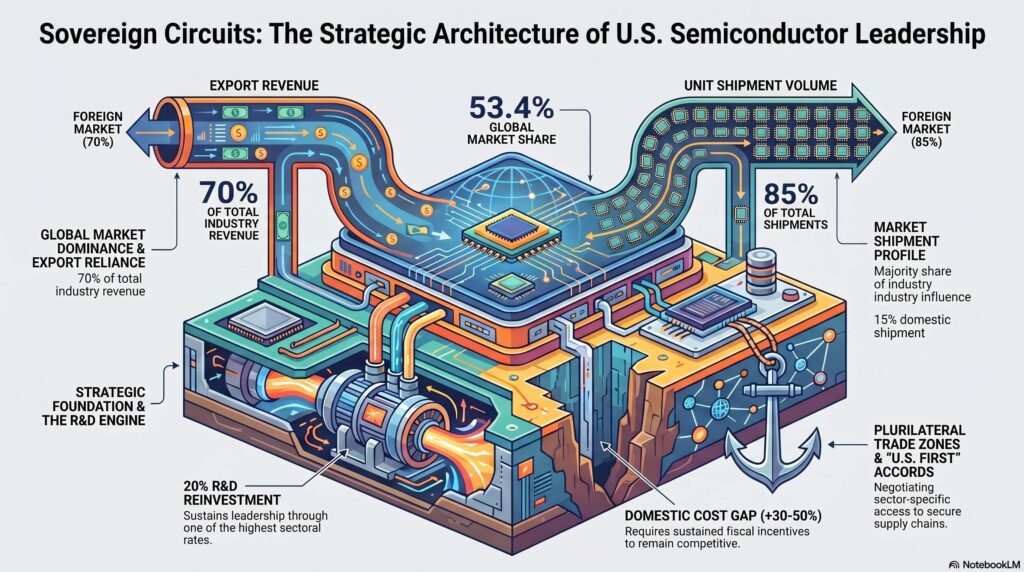

U.S. Leadership

The U.S. semiconductor industry maintains a leading position. It holds a 53.4% market share of global semiconductor sales in 2025. Therefore, any U.S. policy intervention should be designed to maintain and strengthen this position.

International Sales

In 2025, just over 70% of the U.S. semiconductor industry’s revenue came from sales to foreign customers. This has driven a U.S. trade surplus in semiconductors for nearly 30 years.

Market Access

However, based on shipment volume, 85% of U.S.-based semiconductor sales are made in foreign markets. Furthermore, without continued access to foreign markets and policy measures designed to boost demand for U.S. chips, U.S. goals to expand domestic capacity may not be economically viable.

Cost Gap

The total costs of building and operating a semiconductor wafer fabrication plant in the United States are historically 30 to 50% higher than in Asia. However, recent tax and other incentives have helped narrow the cost gap and should be maintained.

R&D Investment

U.S. sales abroad further enable the U.S. semiconductor industry to reinvest an average of approximately 20% of its revenue in research and development (R&D). In fact, this is one of the highest rates in any sector.

In light of this, the goal of U.S. trade policy should be to promote the export and sale of semiconductors produced in the United States. Furthermore, it should also include the global sale of semiconductors by U.S.-based companies.

To this end, the SIA recommended that the USTR pursue a plurilateral agreement on semiconductor trade with like-minded partners and allies. Such an agreement would establish a preferential trade zone free of market distortions. This would strengthen the resilience of semiconductor supply chains and the downstream industries that depend on them.

This initiative is consistent with the Trump Administration’s “America First” Trade Policy Memorandum, which directed the USTR to “identify countries with which the United States can negotiate sector-specific agreements to secure access to export markets.”

Finally, this sector-specific approach is also in line with the USTR’s Trade Policy Agenda 2026, which emphasizes the need for “targeted interventions to support critical sectors,” including semiconductors and semiconductor equipment.