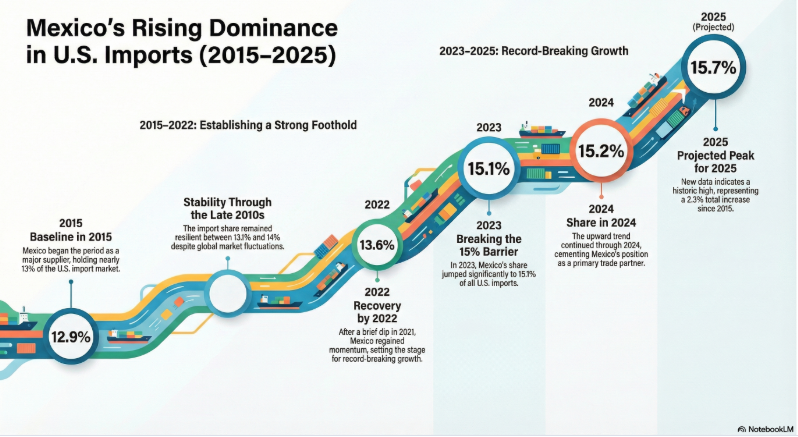

Mexico’s share of imports to the United States reached a historic high for the third consecutive year, rising from 15.5% in 2024 to 15.7% in 2025, with a value of US$534.874 billion, according to the U.S. Department of Commerce.

This progress confirms the structural strengthening of the bilateral relationship under the framework of the United States-Mexico-Canada Agreement.

Record market share in a tariff environment

The increase consolidates an upward trend compared to the 12.9% recorded in 2015. In year-on-year terms, Mexico expanded its share in a global context of increased protectionism and adjustments in U.S. trade policy.

In November 2025, Mexican goods faced an effective tariff rate of 3.7%, substantially lower than the 30.9% applied to China and the 8.1% applied to the European Union. This tariff gap reinforced the relative competitiveness of Mexican exports within North American supply chains.

USMCA review and coordination on critical minerals

The trade dynamics are occurring in parallel with the joint review of the USMCA scheduled for July 2026. On January 29, 2026, President Claudia Sheinbaum and President Donald Trump discussed the terms of this institutional evaluation.

Similarly, on February 4, 2026, the Office of the United States Trade Representative announced a bilateral Action Plan on Critical Minerals. The mechanism seeks to mitigate vulnerabilities in strategic supply chains through coordinated policies, possible adjusted minimum prices at the border, and an eventual binding plurilateral agreement.

Implications for nearshoring and foreign direct investment

Mexico’s repositioning in imports to the United States is partly a response to the phenomenon of nearshoring, which has encouraged the relocation of manufacturing to North America. Sectors such as automotive, electronics, and machinery are seeing growing flows of foreign direct investment linked to regional productive integration.

However, the sustainability of this progress will depend on regulatory factors. These include US tariff adjustments, Mexican trade policy toward third markets, and the results of the USMCA review. These elements have a direct impact on long-term corporate decisions.

Economic growth and macro environment

The Mexican economy grew 0.8% in 2025. For 2026, the International Monetary Fund projects an expansion of 1.5%, conditional on the external environment and trade stability. Moderate growth could limit the dynamism of intermediate imports and the expansion of installed export capacity.

In this context, what risks does Mexico face in its imports to the United States? Mainly, tariff volatility, sectoral trade disputes, and possible changes in rules of origin. What opportunities are emerging? Greater regional integration in critical minerals and strengthening of strategic value chains.