Corn production and imports in Mexico will equal 26 million tons during the 2025-2026 marketing year, which began in October, according to projections by the U.S. Department of Agriculture. The data confirms the country’s persistent external dependence in a context of pressure on agri-food supply chains and regional trade policy.

Year-on-year, production would grow by 11.6%, while imports would increase by 0.3%. In absolute terms, Mexico will maintain a structural balance where foreign trade compensates for insufficient domestic production. This dynamic has a direct impact on tariffs, trade agreements, and supply strategies under the USMCA.

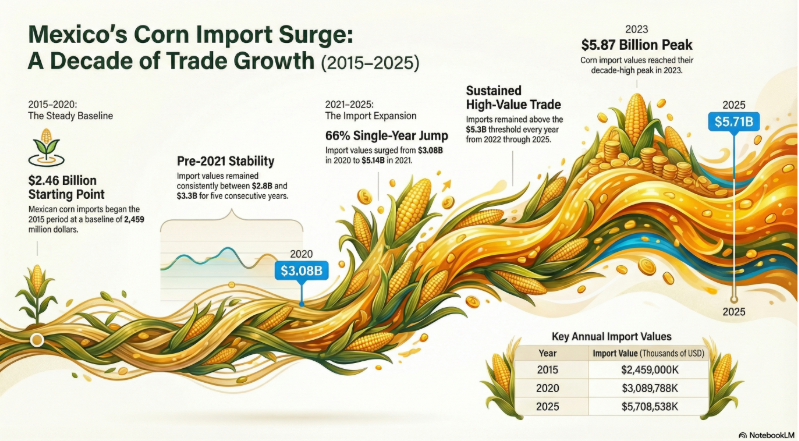

In the last decade, Mexican corn imports grew 132%, from $2.459 billion in 2015 to $5.709 billion, according to data from Banxico. However, this figure is lower than U.S. exports of this grain to the Mexican market, according to USDA statistics.

Agri-food foreign trade and structural dependence

Domestic production is insufficient to meet the growing demand for corn for human consumption and animal feed. Population growth and the expansion of the poultry, pork, and livestock sectors are driving the structural deficit.

Domestic production is insufficient to meet growing demand for corn for human consumption and animal feed. Population growth and the expansion of the poultry, pork, and livestock sectors are driving the structural deficit. Therefore, foreign trade is consolidating its role as a mechanism for stabilizing the domestic market.

Mexico will import 26 million metric tons (MMT) in 2025-2026. Yellow corn will account for about 97% of the total, due to its higher energy content, competitive prices, and continuous availability. In addition, cross-border rail infrastructure favors economies of scale in logistics and reduces transportation costs.

Yellow corn, supply chains, and agro-industrial nearshoring

The predominance of imported yellow corn responds to industrial efficiency criteria. Productive integration in North America strengthens regional supply chains, particularly under the United States-Mexico-Canada Agreement. Current trade policy limits tariff risks and provides regulatory certainty.

The United States supplies more than 99% of Mexico’s corn imports. This pattern deepens bilateral agri-food interdependence. At the same time, regulatory adjustments regarding genetically modified corn have affected the trade in white corn, expanding external flows for industrial use.

Global context: production concentration and futures markets

On an international scale, corn production is highly concentrated. The United States accounts for approximately 33% of global production, followed by the People’s Republic of China. This structure increases the market’s sensitivity to climate variations, geopolitical tensions, and changes in agricultural policy.

In the United States, corn is traded on the Chicago Board of Trade through 5,000-bushel futures contracts with physical settlement. The reference months are March, May, July, September, and December. This market influences international prices and, by extension, import costs for Mexico.

Strategic implications for investment and trade policy

The balance between production and imports raises key questions for Mexico’s agro-industrial strategy. Are there sufficient incentives to increase domestic productivity? How do input costs, recurring drought, and limited infrastructure impact agricultural competitiveness?

From the perspective of foreign direct investment and nearshoring, a stable supply of grains is a critical factor for animal protein and processed food industries. Certainty in foreign trade and rules of origin within North America reduces operational risks for multinational corporations.

However, high external dependence exposes the country to exchange rate volatility, logistical disruptions, and possible adjustments in US trade policy. Consequently, supplier diversification and agricultural modernization are emerging as strategic variables in the medium term.