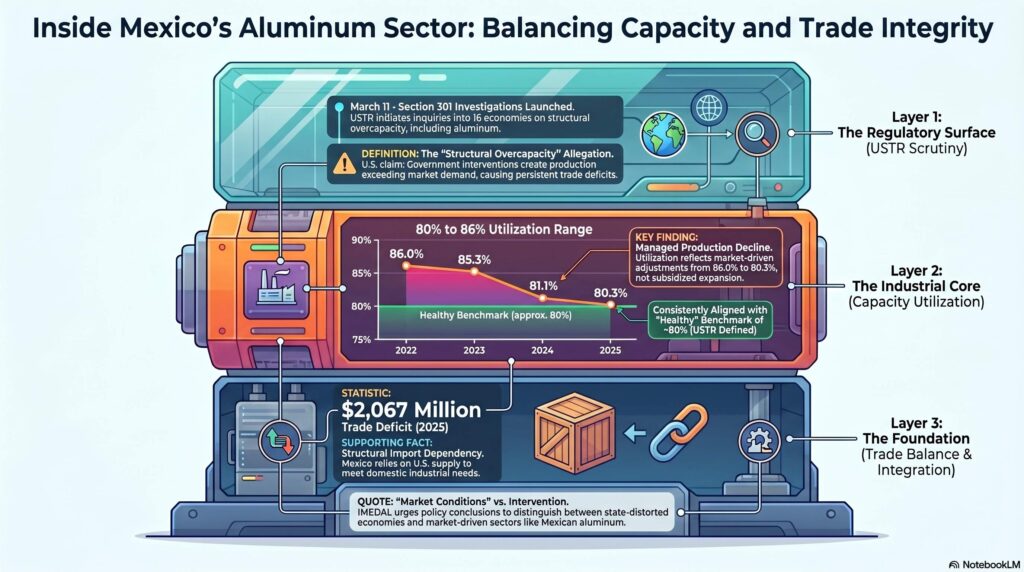

Mexico reduced its aluminum industrial capacity utilization from 86.0% in 2022 to 80.3% in 2025, according to data from the Mexican Aluminum Institute (IMEDAL).

This trend comes as the U.S. Trade Representative (USTR) launched a series of ex officio Section 301 investigations last March into 16 laws. It is also reviewing economic policies and practices related to structural overcapacity and production in the manufacturing sectors.

Aluminum Industrial Capacity

Regarding manufacturing overcapacity, this investigation examines “structural overcapacity” in 16 economies, including Mexico. Furthermore, the United States alleges that government interventions have led to production levels (particularly in automobiles, steel, and electronics) that exceed market demand. This results in persistent trade deficits.

Average aluminum industrial capacity utilization in Mexico fell from 86.0% in 2022 to 85.3% in 2023. It then increased from 81.1% in 2024 to 80.3% in 2025.

Among other points, the USTR’s research notes that healthy capacity utilization rates in manufacturing sectors typically hover around 80%. For example, the average annual capacity utilization in Mexico’s aluminum industry has consistently remained in line with this benchmark. It has ranged from approximately 80% to 86% during the 2022–2025 period.

IMEDAL recognizes the importance of addressing global overcapacity when it is driven by government interventions and creates distortions in production and trade. However, it urged that any policy conclusions distinguish between economies where such conditions exist and those operating under market conditions.

Trade Balance

The Mexican aluminum sector does not have trade surpluses with the United States.

The current USTR investigation links structural overcapacity to sustained trade surpluses driven by government policy interventions. This condition does not exist in the Mexican aluminum sector, according to IMEDAL.

Mexico maintains a consistent aluminum trade deficit with the United States ($2.067 billion in 2025), indicating that domestic production does not exceed demand and that Mexico relies on U.S. supplies to meet its needs. Therefore, IMEDAL argued that this trade pattern is inconsistent with the notion that excess capacity drives exports.

In other words, Mexico is structurally dependent on imports from the United States. This reflects an integrated and complementary North American supply chain.

IMEDAL considered that any disruption to trade in Mexico’s aluminum sector would be detrimental to the highly integrated North American supply chain and could undermine the two countries’ shared economic interests. “Continued collaboration is essential to strengthening regional competitiveness and the growth of the aluminum industry,” it said.