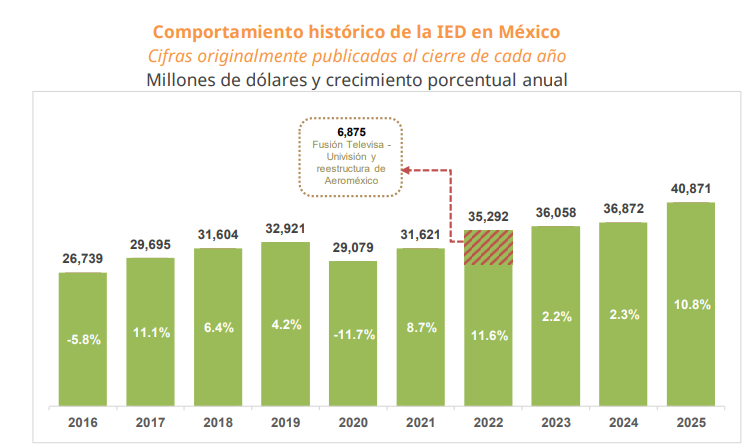

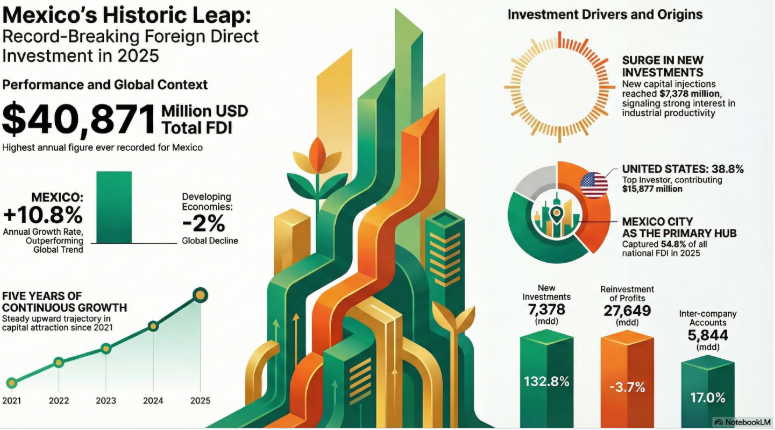

Mexico attracted US$40.871 billion in Foreign Direct Investment (FDI) in 2025, representing year-on-year growth of 10.8%, according to the Ministry of Economy.

The data confirms five consecutive years of expansion, excluding atypical operations, and consolidates the country as a strategic hub for foreign trade and supply chains in North America.

The result takes on greater relevance in an adverse global context. According to the United Nations Conference on Trade and Development (UNCTAD), FDI flows to developing economies fell 2% in 2025.

Foreign Direct Investment in Mexico hits record high in 2025, marking five years of growth

Reinvestment of profits accounted for 67.7% of the total, with $27.65 billion, although it registered a 3.7% year-on-year contraction, derived from higher dividend distributions. This component reflects the permanence of foreign capital and the consolidation of existing operations.

At the same time, new investments grew by 132.9% to US$7.378 billion. This dynamism is the most relevant signal for nearshoring, as it implies fresh capital associated with capacity expansions, technology adoption, and new plants linked to trade agreements and supply chain relocation.

Intercompany accounts amounted to $5.844 billion, an annual increase of 17.0%. This item reflects intragroup financial restructuring and debt movements between parent companies and subsidiaries, which are common in environments of trade policy adjustment and corporate tax optimization.

What happened in the fourth quarter?

During the fourth quarter, there was a negative flow of $5.026 billion, mainly due to dividend payments and financial transactions with affiliates abroad. These were not investment cancellations. The annual net adjustment was marginal (-$35 million), without altering the positive trend.

Country of origin: North America consolidates its leadership

The United States remained the main investor, with $15.877 billion, equivalent to 38.8% of the total. It was followed by Spain (10.8%), Canada (8.1%), the Netherlands (5.8%), and Japan (5.6%). These five economies accounted for 69.1% of the total flow.

Together, the United States and Canada accounted for 46.9% of FDI received, reinforcing regional integration under the USMCA framework and the nearshoring strategy. This concentration suggests a deepening of North American supply chains in the face of geopolitical tensions and global tariff adjustments.

Geographical distribution: concentration in industrial and financial hubs

Mexico City attracted US$22.381 billion, equivalent to 54.8% of the total, with annual growth of 55.1%. This performance reflects its role as a corporate and financial center, where holding and reinvestment operations are registered.

Nuevo León ranked second with US$3.628 billion and 72.9% year-on-year growth, driven by advanced manufacturing and industrial relocation. The State of Mexico ranked third, with US$3.279 billion and an increase of 24.1%.

The five entities with the highest inflows accounted for 80.2% of the national total. This pattern reveals high territorial concentration and raises questions about logistics infrastructure, energy availability, and regional industrial policy.

Implications for foreign trade and trade policy

The performance of Foreign Direct Investment in Mexico confirms the country’s resilience as an export platform. The methodology applied follows the standards of the Organization for Economic Cooperation and Development and the International Monetary Fund, which strengthens international comparability.

For CEOs and foreign trade directors, the record FDI raises strategic questions: Which sectors will attract the most capital in 2026? How will US tariffs and trade policy influence this? What regulatory risks could affect reinvestment? The trend suggests clear opportunities in manufacturing, logistics, and export-related services.